The Sustainable Development Goals, integrated thinking and the integrated report

This publication from the International Integrated Reporting Council (IIRC) and ICAS (the professional accountancy body), in partnership with the Green Economy Coalition has been developed to help organisations enhance their contribution to the SDGs, whilst reducing corporate risk and increasing opportunities that arise from sustainable development issues.

This publication from the International Integrated Reporting Council (IIRC) and ICAS (the professional accountancy body), in partnership with the Green Economy Coalition has been developed to help organisations enhance their contribution to the SDGs, whilst reducing corporate risk and increasing opportunities that arise from sustainable development issues.

The report, authored by academic Professor Carol Adams, is centred on the concept of the six capitals, which is a fundamental feature of Integrated Reporting. It addresses how, through efforts to transforms the capitals to create value for themselves and for others, organisations can make a material contribution to the SDGs, as well as clarify how they are mitigating or alleviating any detrimental effects.

- Download the full publication

- Download the summary version.

The benefits of this document

-

- This publication aims to contribute to the achievement of the SDGs by demonstrating how the International <IR> Framework can help organisations align their contribution to the SDGs with how they create value.

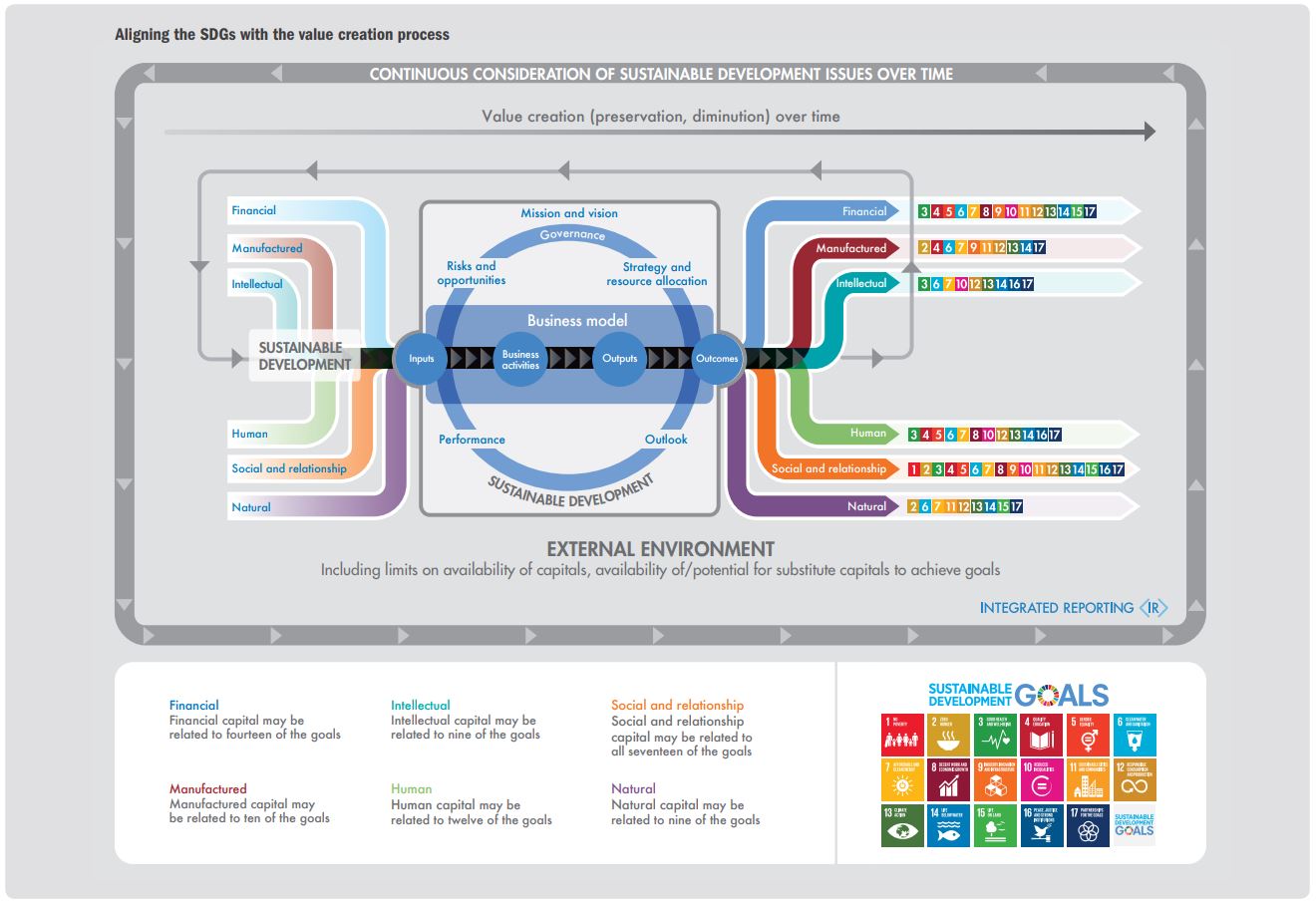

The sustainable development issues which gave rise to the Sustainable Development Goals pose limitations on the availability of capitals on which businesses rely. This framework is aligned with the multi-capital International <IR> Framework issued by the International Integrated Reporting Council.

Through its emphasis on connectivity and Board oversight, it facilitates high-level engagement and a holistic approach (integrated thinking).

Using this framework, organisations will be able to:

- Contribute to the achievement of the SDGs through the application of integrated thinking

- Use integrated reports to communicate their contribution to the SDGs and how they have responded to the risks and opportunities of sustainable development.

This document does not develop indicators or prioritised disclosures to report contributions to the SDGs. Rather it draws on the concepts, guiding principles and content elements of the <IR> Framework and its notion of integrated thinking to help organisations respond to the SDGs.

The document will help organisations that prepare integrated reports in:

- Bringing consideration of the SDGs into mainstream thinking, strategizing, decision making and reporting

- Developing integrated thinking that recognises the risks and opportunities posed by sustainable development considerations

- Identifying solutions that are consistent with sustainable development and which optimise value creation across multiple capitals without depleting capitals which are essential for global sustainable development

- Communicating the relevance of sustainable development to value creation and to an organization’s sustainable development outcomes

- Managing the complexity imposed by sustainable development challenges

- Informing and challenging institutionalized practices and frameworks of government, education and business.

Further information

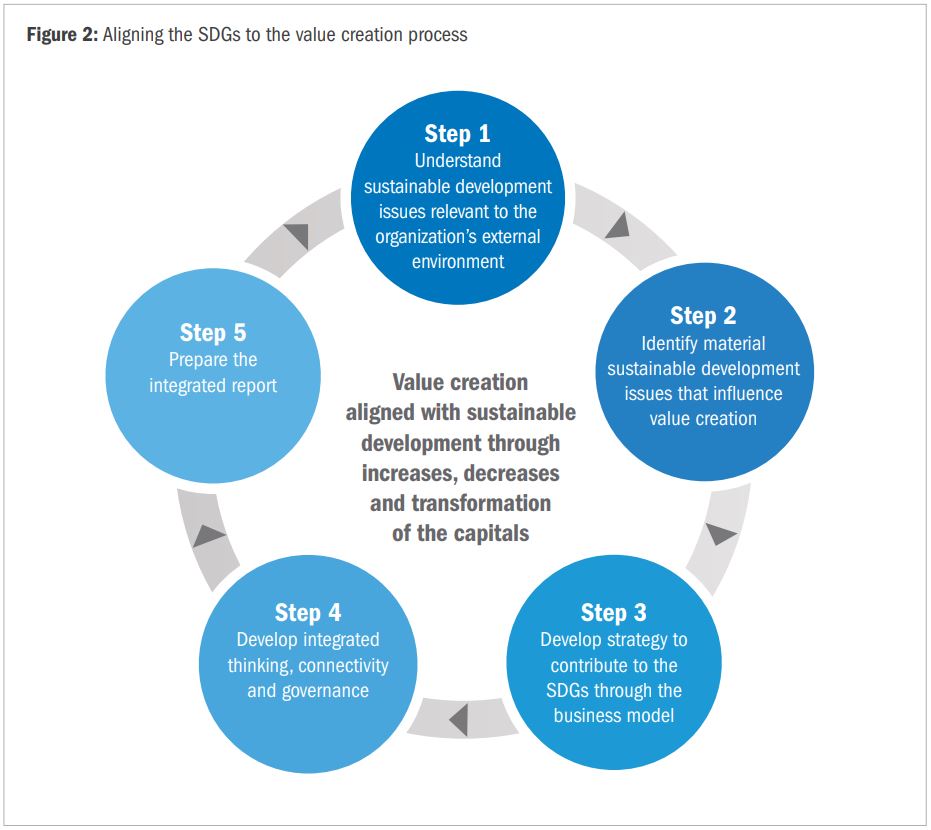

- Understand the framework for contributing to the SDGs through the <IR> value creation process

- Examples of companies that have reviewed the SDGs against their strategy in order to prioritise their efforts to contribute to them.

Who should use this document

This document is aimed at those seeking to enhance the contribution to the SDGs by organisations and those seeking to reduce corporate risk and increase opportunities arising from sustainable development issues. It is particularly relevant to organisations seeking to maximise value creation over the long term and to reassess their mission and purpose.

Within these organisations it is intended for those responsible for developing strategy, those responsible for corporate reporting and to boards. The document is also relevant to those seeking to hold companies to account – investors, regulators, governments, NGOs and other corporate stakeholders – and, of course, to current and potential users of integrated reports.