A shared vision for a comprehensive, globally accepted corporate reporting system

Today, the IIRC has joined forces with CDP, CDSB, GRI and SASB to provide a shared vision for a comprehensive, globally accepted, corporate reporting system that includes both financial accounting and sustainability disclosure connected via integrated reporting.

There has never been a more important time for the principles and concepts of integrated reporting to be embedded within the structure of corporate reporting and the global system of decisions, incentives and asset allocation to achieve financial stability and sustainable development.

This year, we have witnessed businesses around the world having to pivot their business models overnight, to prioritise the health and safety of their employees and customers above the immediate financial success of the business. The connectivity between sustainability-related factors and immediate financial-viability is clearer than ever before.

It is why we are committed to working with our partners to drive a holistic system for reporting across the value chain.

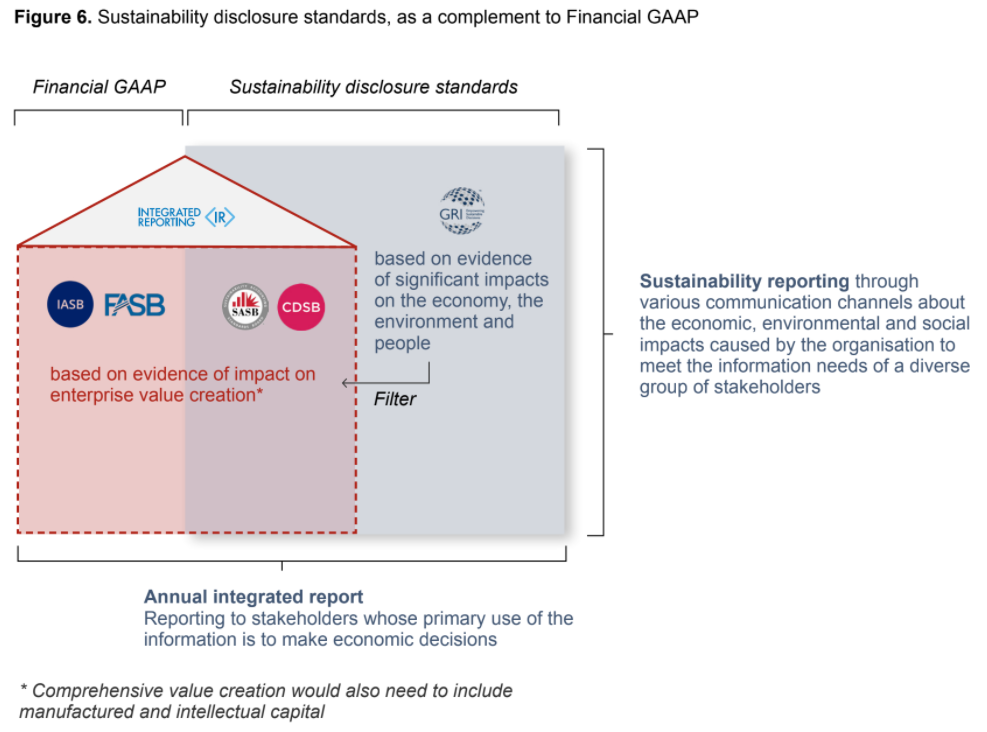

We know that businesses globally are already using a mixture of frameworks and standards to provide stakeholders with robust, effective information to drive better decision-making and capital allocation via their integrated report.

Integrated reporting has been adopted by more than 2,000 organisations in more than 70 markets and many of these businesses already use the GRI and/or SASB standards to develop the metrics and indicators that is then used to inform their integrated thinking, resource allocation decisions and ultimately their integrated report.

The paper sets out how sustainability disclosure that is material for enterprise value creation should ideally be disclosed along with information that is already reflected in the annual financial accountants. Integrated reporting provides the conceptual framework linking such disclosures.

We know that there is a lot of interest from the business, investor and regulatory community in obtaining a single standard for sustainability reporting. The European Commission has recently appointed a task force through EFRAG on Preparatory Work for the Elaboration of Possible EU Non-Financial Reporting Standards. IOSCO, IFRS and the World Economic Forum are others that are active in this space.

The IIRC’s message to these organisations is yes, we agree with you that there needs to be a harmonised system for reporting. And yet, the four organisations that we have partnered with today (CDP, CDSB, GRI, SASB) represent the overwhelming majority of quantitative and qualitative sustainability disclosures today, and they each recognise the role the International Integrated Reporting Framework plays already in connecting sustainability disclosure to reporting on financial and other capitals.

We are therefore calling on these regulatory and international organisations to avoid placing new burdens on companies by creating new standard, but to work with us and the other standard setters, using this paper as a building block, to deliver a new comprehensive system.

Climate change, the global pandemic and the growing infrastructure gap globally are all clear signs that the world cannot wait much longer.